In 2026, the global energy landscape is defined by its inherent vulnerability to sudden shocks. As a proof point of this volatility, we have seen Brent Crude markers surge to 120 USD/barrel during periods of tension and natural gas prices across Europe and Asia remain significantly above historical averages. The global economy is managing a geopolitical risk premium characterised by pronounced price fluctuations.

Source: The Guardian (7 April 2026)

Oil has largely vanished from European electricity generation; however, countries such as Italy, the Netherlands, and the UK still rely heavily on gas to power their grids. Other major industrial economies, including Germany and Poland, also use gas primarily as a flexibility fuel (International Energy Agency). However, any liquefied natural gas (LNG) disruption due to recent tensions in the Middle East does not immediately affect day-ahead power prices in Europe. Shipments typically take weeks to reach Europe with many ongoing shipments already contracted. In addition, Europe has significant gas storage that buffers short-term shocks.

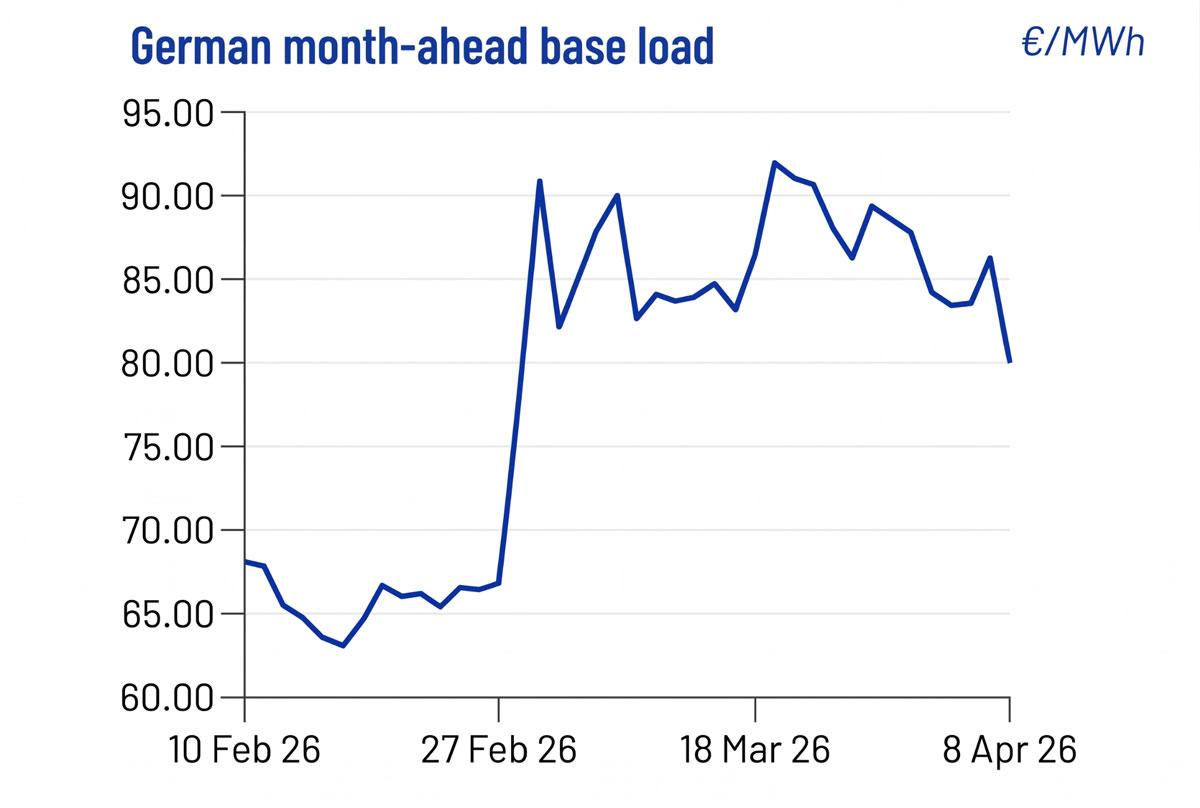

However, markets react first through expectations in gas pricing rather than physical shortages, which means price changes show up in forward contracts before spot markets. These early signals are already visible in forward markets. In products such as month-ahead contracts, buyers and sellers are positioning themselves for potential price shocks.

Source: Argus Media

Beyond political tensions and the resulting fuel price shocks, weather-driven supply variability, grid congestion, and accelerating demand from electrification and digitalisation have all contributed to a sustained rise in energy market volatility. In this environment, corporate Power Purchase Agreements (PPAs) are emerging as a critical financial and operational hedge. Corporate PPAs offer long-term price certainty and protection against wholesale electricity fluctuations.

For businesses, the message is clear: securing renewable energy procurement, such as Power Purchase Agreements (PPAs) and long-term Energy Attribute Certificates (EACs), has evolved from a sustainability goal into a critical tool for long-term strategic hedge.

Strategic procurement focuses on reducing exposure to external power supply and renewable certificate price disruptions through two primary mechanisms: Power Purchase Agreements (PPAs) and long-term Energy Attribute Certificate (EAC) Agreements.

By signing a long-term PPA, a company secures electricity prices for a decade or more, mainly 10 to-20 years, offering protection against wholesale electricity fluctuations.

This approach also strengthens energy independence. By directly sourcing power from local wind or solar projects, companies reduce their exposure on volatile global commodity markets that are driven by fossil fuel price swings. Corporate PPAs tied to domestic renewable generation are therefore becoming a way to localise and stabilise energy supply.

The business case for long-term renewable energy agreements is also driven by the structural pricing dynamics of PPAs. While the renewable sector faces its own challenges, such as the price of steel and copper, there is a structural advantage: Unlike wholesale electricity prices, which are heavily influenced by short-term fuel costs and market sentiment, PPA prices are based primarily on the levelized cost of electricity (LCOE) of the underlying asset.

In an environment of rising energy costs, this "pricing lag" between the short- and mid-term volatility of wholesale electricity prices and the long-term prices achieved through PPAs allows organisations to materialise cost savings by locking in rates that remain insulated from grid volatility.

For organisations where a corporate PPA is not immediately feasible, long-term EAC contracts, which typically range 3 to 5 years, can offer an alternative strategic hedge to mitigate certificate price risks. As the GHG Protocol and SBTi evolve toward greater emphasis on 24/7 renewable energy matching and geographical granularity, these long-term EACs contracts can also become a cost-effective tool to meet heightened requirements and secure sustainability targets. We see an increased demand for long term EAC contracts with the option of 24/7 matching in case of materialised updates from SBT and the GHG Protocol.

While corporate PPAs are ideal for securing price and electricity over a 10-to-20-year tenor, long-term Energy Attribute Certificate (EAC) contracts can also be layered on top of the secured PPA supply to provide volume flexibility for the mid-term horizon. This combination allows organisations to balance long-term price certainty with shorter-term adaptability as demand profiles, regulatory requirements, or market conditions evolve.

While the pathway to long-term hedge against volatility is clear, the transition is a significant strategic shift that requires deep internal coordination.

The implications of remaining in a “wait and see” approach are material: without long-term fixed contracts, organisations remain fully exposed to market volatility. For energy-intensive sectors like data centers, heavy manufacturing, and chemicals, energy procurement is now a core component of maintaining operational stability.

We are also observing potential regional price lags in markets like ASEAN and LATAM. While industrial consumers in these regions may currently feel insulated by government subsidies or regulated tariffs, these fiscal buffers are facing increasing pressure. As generation costs rise, the transition toward market-reflective pricing may result in abrupt adjustments for industrial users. Furthermore, the regulatory environment is evolving as governments prioritise domestic energy production and tighten climate disclosure requirements.

Success in the current market requires a structured approach to procurement, built on three pillars:

The transition toward renewables is increasingly driven by risk management. Resilient companies view renewable energy as a strategic asset. By prioritising price certainty and supply stability, businesses can establish the financial foundation necessary to navigate an unpredictable global market.

Contact our Renewable Energy Advisory team today to discuss how South Pole can help you design a procurement strategy that protects your operations and secures your energy future.