In the European Union, the approval of the Corporate Sustainability Reporting Directive (CSRD) is set to bring about a step change in corporate sustainability disclosures and performance assessment.

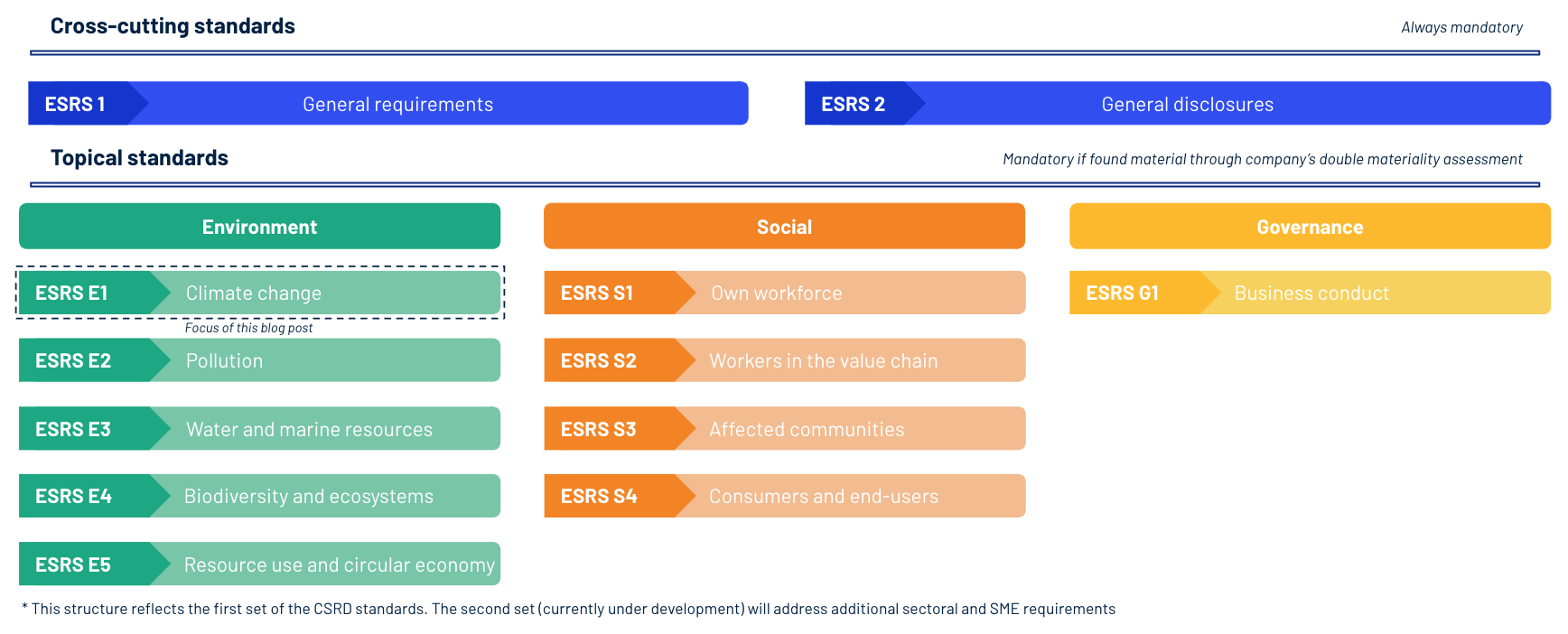

The CSRD, successor to the Non-Financial Reporting Directive (NFRD), presents a powerful lens through which companies must disclose their environmental and social impacts, assess their strategic and financial implications, and communicate their responses. The first set of CSRD standards includes two cross-cutting standards and ten topical standards that companies must report against according to a double materiality assessment.

This blog focuses on the Climate Change topical standard of the CSRD, known as ESRS E1. Specifically, it explores the requirements for identifying and assessing climate change risks and opportunities and their integration into business resilience planning. It aims to support businesses' first steps towards compliance with these aspects.

Cross-cutting and topical standards of the CSRD

ESRS E1 on Climate Change aims to provide investors and wider stakeholders with an understanding of both how the disclosing company affects climate change and how climate change impacts the company itself. In recent years, many companies have made advancements in understanding and managing the impacts they have on climate change through greenhouse gas (GHG) accounting, (science-based) target setting (SBTs), and mitigation actions. However, fewer companies have assessed and disclosed how climate change will likely affect their operations and financial performance in the short, medium, and long term, making this a priority for companies seeking to comply with the CSRD.

|

Reference |

Disclosure Requirement |

|

ESRS 2 - GOV 3 - E1 |

Integration of sustainability related performance in incentive schemes |

|

ESRS E1-1 |

Transition plan for climate change mitigation |

|

ESRS 2 - SBM 3 - E1 |

Material impacts, risks and opportunities and their interaction with strategy and business model |

|

ESRS 2 - IRO 1 - E1 |

Description of the processes to identify and assess material climate-related impacts, risks and opportunities |

|

ESRS E1-2 |

Policies related to climate change mitigation and adaptation |

|

ESRS E1-3 |

Actions and resources in relation to climate change policies |

|

ESRS E1-4 |

Targets related to climate change mitigation and adaptation |

|

ESRS E1-5 |

Energy consumption and mix |

|

ESRS E1-6 |

Gross Scopes 1, 2, 3 and Total GHG emissions |

|

ESRS E1-7 |

GHG removals and GHG mitigation projects financed through carbon credits |

|

ESRS E1-8 |

Internal carbon pricing |

|

ESRS E1-9 |

Anticipated financial effects from material physical and transition risks and potential climate-related opportunities |

ESRS E1 Disclosure requirements for climate change risks and opportunities, financial impacts, and responses

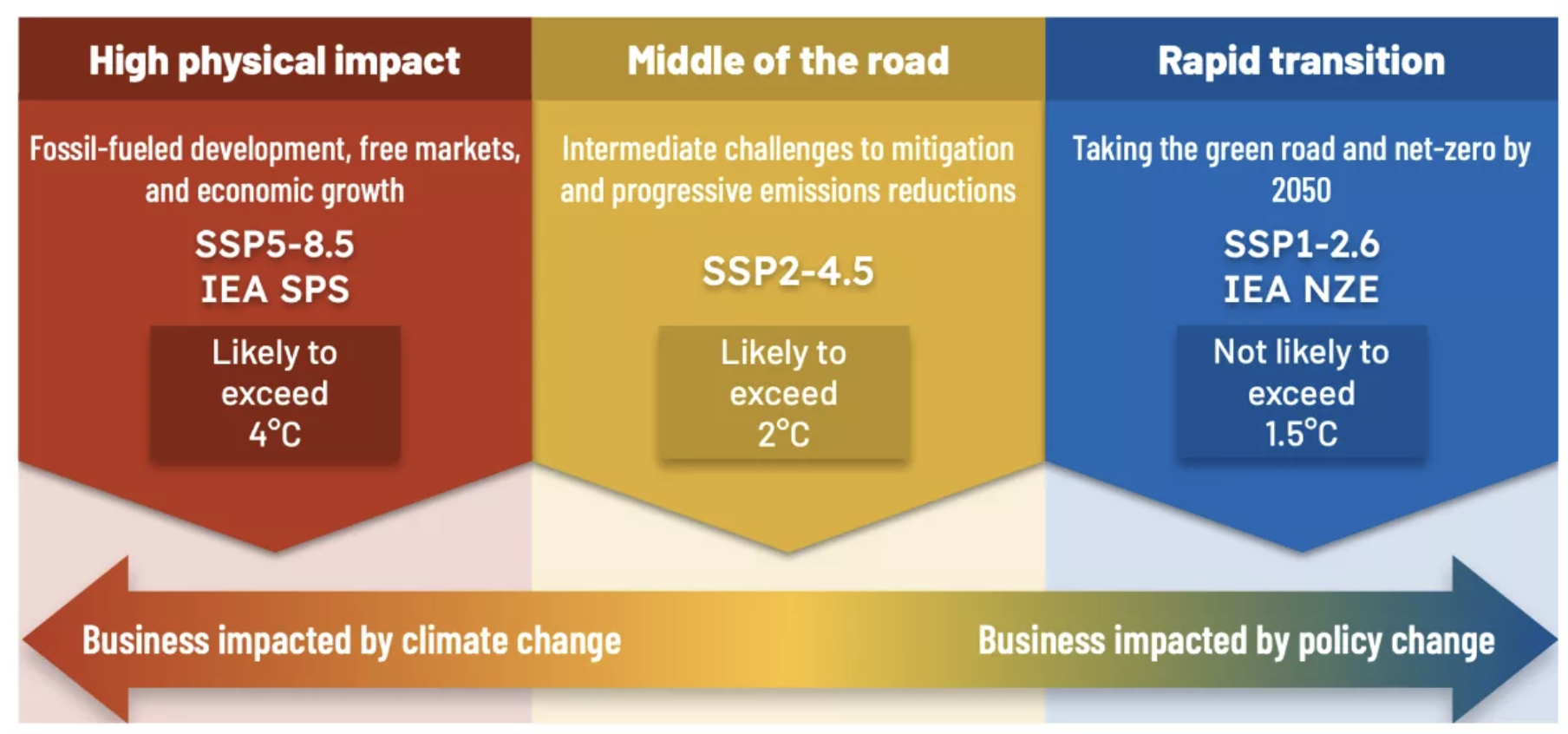

The first step when seeking to comply with ESRS E1's risk-related disclosure requirements is to identify the material climate risks and opportunities for the business. Given the uncertainties in the evolution of global GHG emissions and their associated climate impacts across different time horizons, the CSRD, in line with the widely used and respected reporting framework from the TCFD (Task Force on Climate-related Financial Disclosures), requires climate-related risks and opportunities to be assessed using scenario analysis. In other words, climate risks and opportunities should be identified by taking a range of possible futures into account, including a 'best case,' a rapid, low-carbon transition where global warming is limited to 1.5°C, as well as a 'worst case', high physical impact scenario of +4°C warming by 2100.

Climate scenarios ranging from ‘high physical impact’ to ‘rapid transition’

Assumes very low political momentum and ambition, with little action on climate change mitigation.

Assumes the world does not rapidly shift from present day social, economic, and political trends. Progress is slow and greenhouse gas emissions do not level off until 2100.

Different climate change scenarios present different types of risks and opportunities. The CSRD classifies these into two main categories: physical risks and opportunities and transition risks and opportunities.

Physical risks are those associated with extreme weather events and long-term changes in weather patterns. While relevant to all scenarios, with effects already being felt today, these risks are most pronounced in a +4℃ warming scenario with limited mitigation action. In this scenario, companies face impacts from (e.g.) increased capital costs associated with asset damage from extreme weather events (e.g., hurricanes, flooding) and reduced revenues and profits due to declining worker productivity and health and safety due to extreme heat conditions.

On the other hand, transition risks and opportunities are those associated with transitioning into an economy that limits global warming, in the optimal scenario, to 1.5°C above pre-industrial levels. Given the stringent climate policies and carbon pricing needed to drive this shift towards a drastically decarbonising global economy, and the necessary transformation in technologies and markets, companies face various potential legal, technological, reputational, and market-related transition risks. However, the low-carbon transition also presents significant opportunities for resource optimisation, cost reduction, and innovation. Under ESRS E1, companies must identify and assess their material transition risks and opportunities, which may include risks from increased operating costs due to the imposition of carbon taxes and more stringent energy and fuel obligations, as well as opportunities arising from increased sales of low-carbon products and services that benefit from much higher customer demand.

ESRS E1 requires companies to identify and assess their material climate change risks and opportunities and quantify their anticipated financial impacts. Specifically, companies need to disclose how climate risks could affect their financial position, performance, and cash flows in different time frames. A significant level of detail is requested: ESRS E1-9 requires companies to disclose 'significant amounts of the assets and net revenue at material physical or transition risk' – and, conversely, potential cost-savings from climate mitigation and adaptation actions, as well as revenue from low-carbon products or services. In other words, the CSRD aims to provide investors and other stakeholders with much more information on how vulnerable a company is to climate change impacts or how it is set to benefit from supporting the low-carbon transition or global adaptation efforts.

Calculating the financial impacts of risks and opportunities is challenging because it entails a range of uncertainties relating to, among other things, climate scenarios and business strategy. It requires close collaboration between internal business units, value chain actors, and climate-change experts to understand how and to what extent climate-related hazards may impact the company's assets, supply chain, profits, or costs.

Recognising these difficulties, the CSRD has established a phased-in approach to disclosing quantified impacts. Companies can disclose qualitative data for the first three years of CSRD reporting, so they may use this time to build up their climate scenario analysis and financial impact quantification to put a solid reporting base in place for their fourth disclosure.

Having identified, assessed, and quantified material climate-related risks and opportunities, ESRS-E1 requires companies to disclose their response to these aspects in the form of climate mitigation and climate adaptation policies and associated actions. Companies must also report their transition plan for climate change mitigation, assuming a 1.5°C pathway. In doing so, companies can demonstrate to investors that material climate risks are being managed and/or opportunities are set to be realised.

It is evident that, beyond being a disclosure regulation, the CSRD provides a valuable framework for future-proofing businesses and ensuring their longevity and relevance in the face of a delayed (and increasingly urgent) low-carbon transition. The climate risk disclosure requirements of ESRS E1 won't be quick or easy to align with but will prompt important internal reflections on the role of business in a changing climate while providing investors and wider stakeholders with a much clearer picture of companies' climate performance, both now and in the future.

Understanding and complying with the CSRD climate risks and opportunity requirements might seem daunting, but it needn't be.

Following a gradual approach can help companies at the beginning of their journey to identify the first steps to take on their road to compliance. In contrast, companies in later stages can focus on more detailed assessments.